Share this Post

Need help with your money or investments? Book a consultation to learn more about working together.

Our Investment Philosophy

If you prefer the short version, our philosophy is simple:

- Follow the evidence, not the hype.

- Buy shares of quality businesses to build wealth.

- Manage risk to preserve wealth.

If you want to understand how we put that into practice, keep reading.

We believe successful investing is not about chasing headlines, predicting the economy, or constantly searching for the next hot idea.

It is about owning productive assets, managing risk thoughtfully, and using a disciplined process that you can stick with over time.

At our firm, our investment philosophy is built around a simple idea: the portfolio should serve the purpose of the money. That means the right investment strategy is not always the most complicated one, nor is it always the one with the highest theoretical return. It is the one that best aligns with your goals, your time horizon, your need for liquidity, and your ability to stay disciplined through uncertainty.

Historically, our client portfolios have been built primarily with our proprietary Quality Core™ strategies, which are grounded in evidence-based research and implemented with ETFs & Mutual Funds.

More recently, we added our Quality Select™ strategy, an optional way to complement the Quality Core™ portfolio with a curated allocation to individual stocks. Quality Core™ remains a complete solution on its own, while Quality Select™ may be appropriate for growth-oriented clients who have a higher tolerance for risk and are comfortable owning individual stocks.

These are different tools, but they are guided by the same principles: quality, discipline, long-term thinking, diversification where appropriate, concentration where justified, and an ongoing focus on managing risk.

Why Investment Philosophy Matters

Most investors have goals. They want to grow their wealth, generate income, preserve what they have built, or avoid unnecessary risk. But goals are not the same as an investment philosophy.

A philosophy defines the principles that guide how those goals are pursued. It helps answer important questions: What do we believe about markets? What types of investments do we want to own? How much risk are we willing to accept? What will we do when markets become uncomfortable?

That matters because investing success is not just about picking good investments. It is also about behavior. Even a sound strategy can fail in practice if an investor abandons it during a difficult stretch. A good advisor can provide meaningful value by helping clients stay disciplined when emotions are high and markets are uncertain.

We believe a good investment philosophy should be understandable, durable, and rooted in common sense. It should provide a framework for making decisions and help investors remain disciplined when fear, greed, or uncertainty try to pull them off course.

At the end of the day, there is no way to know with certainty whether one strategy will outperform another in the future. That is why we believe it is important to choose a strategy you genuinely understand and believe in. If you save consistently, invest prudently, avoid emotional trading, and stay committed to a sound process, you are already doing many of the things that matter most for success.

Our Quality Core™ Portfolios

Our Quality Core™ portfolios are the foundation of our investment approach.

They are built primarily with ETFs and are grounded in evidence-based investing, often referred to as factor investing.

That phrase can sound technical, but the idea is straightforward. Over many decades, academic research has found that certain characteristics, or factors, have historically been associated with higher expected returns across broad groups of stocks.

Importantly, this is not traditional stock picking. With factor investing, you are not trying to identify a single company that will outperform. You are investing in a diversified bundle of stocks that share a certain characteristic you want exposure to.

This allows us to build portfolios that are broad, intentional, and grounded in long-term evidence rather than short-term predictions.

Our Quality Core™ portfolios emphasize four factors we believe are particularly sensible and durable:

- Market

- Size

- Value

- Quality

Now that we’ve introduced the idea of evidence-based investing, the next step is to discuss the specific factors we focus on and how each one is intended to improve the portfolio.

The Factors We Focus On

Market

The market factor is the most intuitive.

It simply means that owning stocks has historically offered higher expected returns than owning bonds or cash over long periods of time. Investors take more risk when they own shares of businesses, and over time they have generally been compensated for that risk.

If stocks did not offer higher long-term expected returns, there would be little reason to accept their additional volatility.

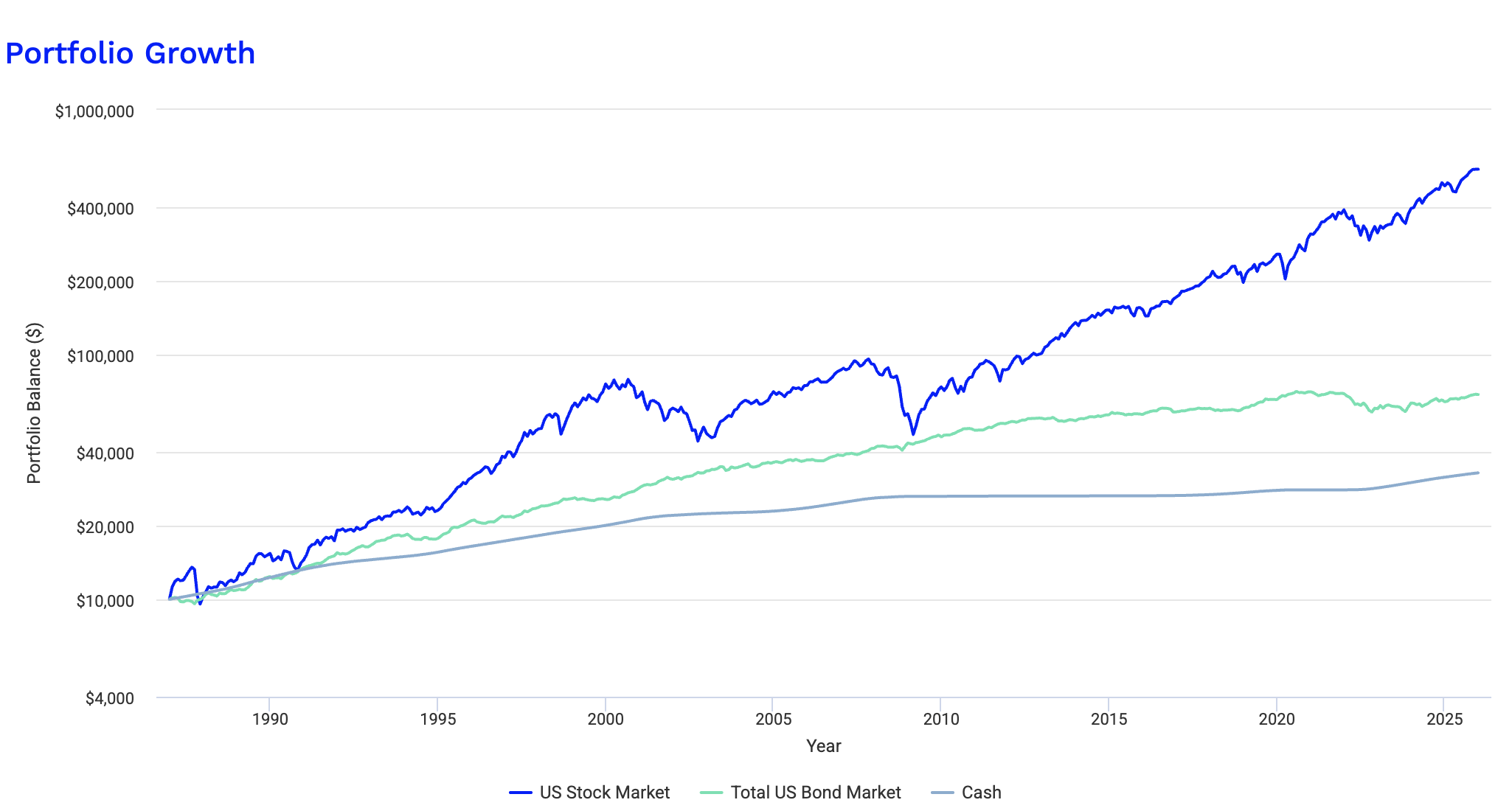

As you can see in the chart below, investing in the United States stock market has historically built significant wealth relative to cash and bonds.

Size

The size factor refers to the historical tendency of smaller companies to outperform larger companies over long periods of time.

Smaller companies are often earlier in their growth journey, less followed, and sometimes priced with greater skepticism. As a group, they have historically offered higher expected returns, though with greater volatility and longer stretches of underperformance.

This is important. Higher expected return does not mean smoother performance. Investors need to be able to tolerate discomfort if they want to benefit from the factor over time.

The chart below shows the growth of a $10,000 investment in both US Large Cap and US Small Cap from January 1972 through December 2025. The ending balance for US Large Cap was $2,613,643 vs $3,437,793 for US Small Cap.

Value

The value factor reflects the idea that cheaper stocks, relative to their fundamentals, have historically outperformed more expensive stocks over the long term.

This does not mean buying poor businesses simply because they look cheap. It means that valuation matters. The price you pay for an investment influences the return you are likely to receive.

Popular and expensive parts of the market can remain strong for long periods, so value investing requires patience. But over full cycles, paying a reasonable price has historically mattered.

We find the value factor particularly compelling when it is combined with the small-cap factor (Size factor).

Using the same timeframe discussed in the previous section, US Small Cap Value ended with a balance of $9,038,604.

Quality

Quality is one of the factors we find especially compelling because it connects academic research with a principle most investors already understand: we would rather own strong businesses than fragile ones.

A quality business is typically one with a strong balance sheet, consistent profitability, thoughtful leadership, durable competitive advantages, and the ability to earn attractive returns on capital over time. In plain English, these are companies that have proven they can make money, manage risk, reinvest wisely, and endure through different economic environments.

That matters because investing is not just about chasing the highest possible return. It is also about owning assets that give you a better chance of staying invested when markets become uncomfortable. Strong businesses are not immune to volatility, but they are often better positioned to adapt, recover, and continue compounding over time.

This is also why the quality factor connects so naturally with the thinking of investors like Warren Buffett and Charlie Munger. Long before “factor investing” became common language in wealth management, they emphasized the value of owning exceptional businesses and giving compounding time to work.

For retirees and those approaching retirement, quality can be especially important. When your portfolio is no longer just about accumulation, but also about supporting income, managing risk, and preserving financial independence, the strength of what you own matters.

Our Quality Select™ Portfolios

Our Quality Core™ portfolios remain the foundation for most clients, and for many, especially those in or near retirement, this is the appropriate long-term solution. It is diversified, disciplined, and designed to support the real-world goals most clients care about: growth, income, risk management, and long-term sustainability.

We added Quality Select™ for clients who want to complement Quality Core™ with a custom, dedicated allocation to individual businesses.

Quality Select™ is an optional portfolio made up of individual stocks. It is designed for clients with a growth focus, a higher tolerance for risk, and sufficient account size to make a concentrated stock allocation appropriate.

With Quality Core™, we are using diversified ETFs to capture broad market and factor exposures. With Quality Select™, we are making more deliberate decisions about which specific companies we believe are worthy of long-term ownership.

That introduces both opportunity and risk.

The opportunity is that a well-selected group of exceptional businesses may outperform over time. The risk is that concentration increases the impact of being wrong.

That is why we do not treat individual stock investing casually. Quality Select™ is not about speculation, story stocks, or reacting to headlines. It is about thoughtful ownership of businesses we believe are high quality, understandable, and capable of compounding value over long periods.

Most clients do not need Quality Select™ to have a successful investment experience. Quality Core™ remains our primary portfolio solution. Quality Select™ exists for clients whose goals, risk tolerance, time horizon, and interest in individual stock ownership make it a reasonable complement to the broader plan.

Investing During Retirement Is Different

Investment philosophy becomes even more important as you approach and enter retirement.

During the accumulation years, the primary objective is often growth. You are adding to the portfolio, time is generally on your side, and market downturns can feel uncomfortable but still manageable.

Retirement changes the equation.

At that point, the portfolio is no longer just something to grow. It may need to help fund your lifestyle, support regular withdrawals, preserve flexibility, provide liquidity, and protect against risks that become more meaningful once the paycheck stops.

That includes sequence risk, or the risk of experiencing poor market returns early in retirement while withdrawals are being taken. It also includes inflation risk, because the income needed to support your lifestyle will likely rise over time. A portfolio that looks safe today may not feel safe years from now if it fails to keep up with rising costs.

This is why we believe retirement portfolios should be evaluated not only by return, but by risk-adjusted return; the amount of return pursued relative to the risk required to earn it. The goal is not simply to chase the highest possible return. The goal is to build a portfolio that gives you a reasonable opportunity to grow, while also helping you stay invested through difficult markets.

That is one reason we believe in purpose-based allocations.

A portfolio should not be a random collection of investments. Each part should have a clear role. The question is not simply, “What should we own?” It is also, “What job is this part of the portfolio supposed to do?”

For example:

- Stocks may help grow purchasing power over time.

- Bonds may help reduce volatility and support spending needs.

- Cash may provide liquidity and flexibility.

- A diversified ETF allocation may provide broad market exposure, discipline, and structure.

- A concentrated stock allocation may provide additional upside potential for dollars earmarked for long-term growth or legacy goals, where the time horizon is longer and the tolerance for volatility is higher.

In retirement, every allocation should have a purpose: supporting income, managing risk, preserving flexibility, growing purchasing power, or funding long-term legacy goals.

A good retirement portfolio is not simply the one with the highest expected return. It is the one designed to support the life the money is meant to fund while managing the risks that could disrupt that life along the way.

Final Thoughts

Our investment philosophy is not built around predicting the next market move or chasing whatever strategy has worked most recently. It is built around discipline, evidence, quality, and the belief that every portfolio should serve a clear purpose. For clients nearing or in retirement, that purpose is especially important: helping support the life they want to live while managing the risks that could get in the way. No strategy can eliminate uncertainty, but a thoughtful, durable investment philosophy can provide the structure needed to stay focused, make better decisions, and remain committed to a sound process over time.

If our philosophy resonates with you, we invite you to schedule a brief introductory call to see if we may be a good fit.

Disclosure

All investing involves risk, including loss of principal. Past performance does not guarantee future results. No investment strategy can guarantee success or protect against loss in all market environments. References to factors such as market, size, value, and quality reflect long-term research and historical observations, but there is no assurance these factors will persist or outperform in the future. Chart data was pulled from various indexes in the Portfolio Visualizer research tool. Any discussion of individual stocks, funds or strategies is for illustrative purposes only and should not be interpreted as a recommendation to buy or sell any security. Investment strategies should always be considered in light of an investor’s own goals, time horizon, liquidity needs, and risk tolerance. Please consult your financial advisor before making any investment decisions.